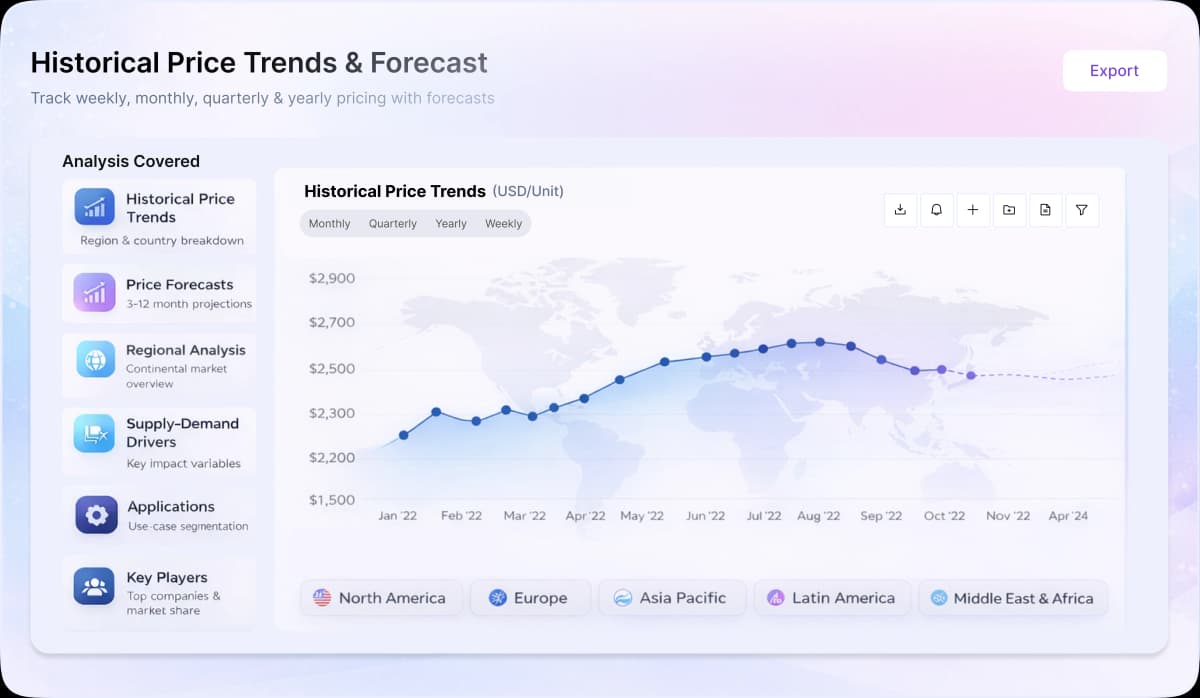

The antimony market in 2025 followed a pronounced “surge–correction–high fluctuation” pattern, driven by structural supply tightness and evolving demand dynamics. Early in the year, prices surged due to tightening mining quotas in China, reduced imports of antimony concentrates, and simultaneous stockpiling from the photovoltaic sector, where antimony is a critical input for solar glass production. This was further intensified by a widening global supply-demand gap and declining ore availability, as environmental restrictions, mine closures, and resource depletion constrained output, particularly in key producing regions such as Hunan and Guangxi. Imports into China dropped significantly, reinforcing raw material shortages and amplifying volatility. However, from Q2 onward, prices corrected amid a temporary demand slowdown, especially due to destocking in photovoltaic glass and weaker consumption in antimony oxide applications. Regionally, North America maintained a firm tone supported by rising industrial production, defense demand, and renewable energy transition trends, alongside constrained supply from global production declines and export restrictions. In contrast, Europe experienced downward pressure in Q4 as energy costs eased and Chinese export licenses improved supply availability, while construction weakness offset gains from automotive recovery. Across Asia, particularly China, improved manufacturing activity and industrial output toward year-end supported a rebound, although weak consumer sentiment and deflationary pressures limited stronger momentum. Overall, persistent supply constraints, shifting trade flows, and demand variability drove elevated yet volatile market conditions throughout the year.